When it comes to financial emergencies, many individuals turn to their 401(k) retirement accounts for assistance. However, the concept of lying to get a 401(k) hardship withdrawal raises significant ethical and legal concerns. Understanding the rules and regulations surrounding hardship withdrawals is crucial for anyone considering this option. In this article, we will explore the implications of dishonesty in the context of 401(k) withdrawals, the legal framework surrounding hardship withdrawals, and the potential consequences of misrepresenting information.

As the financial landscape becomes increasingly complex, the temptation to bend the rules can be strong. However, it is essential to recognize that the consequences of lying can be severe, both financially and legally. This article aims to provide comprehensive insights into the 401(k) hardship withdrawal process, the importance of honesty, and the potential repercussions of dishonest actions.

Whether you are in a financial bind or simply seeking information for the future, this guide will equip you with the knowledge necessary to navigate the complexities of 401(k) hardship withdrawals responsibly. Let’s delve into the details and clarify the importance of maintaining integrity in financial matters.

Table of Contents

- Understanding 401(k) Hardship Withdrawals

- Eligibility Requirements for Hardship Withdrawals

- The Role of Employers in 401(k) Hardship Withdrawals

- Consequences of Lying to Get a Hardship Withdrawal

- Alternatives to Hardship Withdrawals

- How to Apply for a Hardship Withdrawal

- Expert Views and Statistics

- Conclusion

Understanding 401(k) Hardship Withdrawals

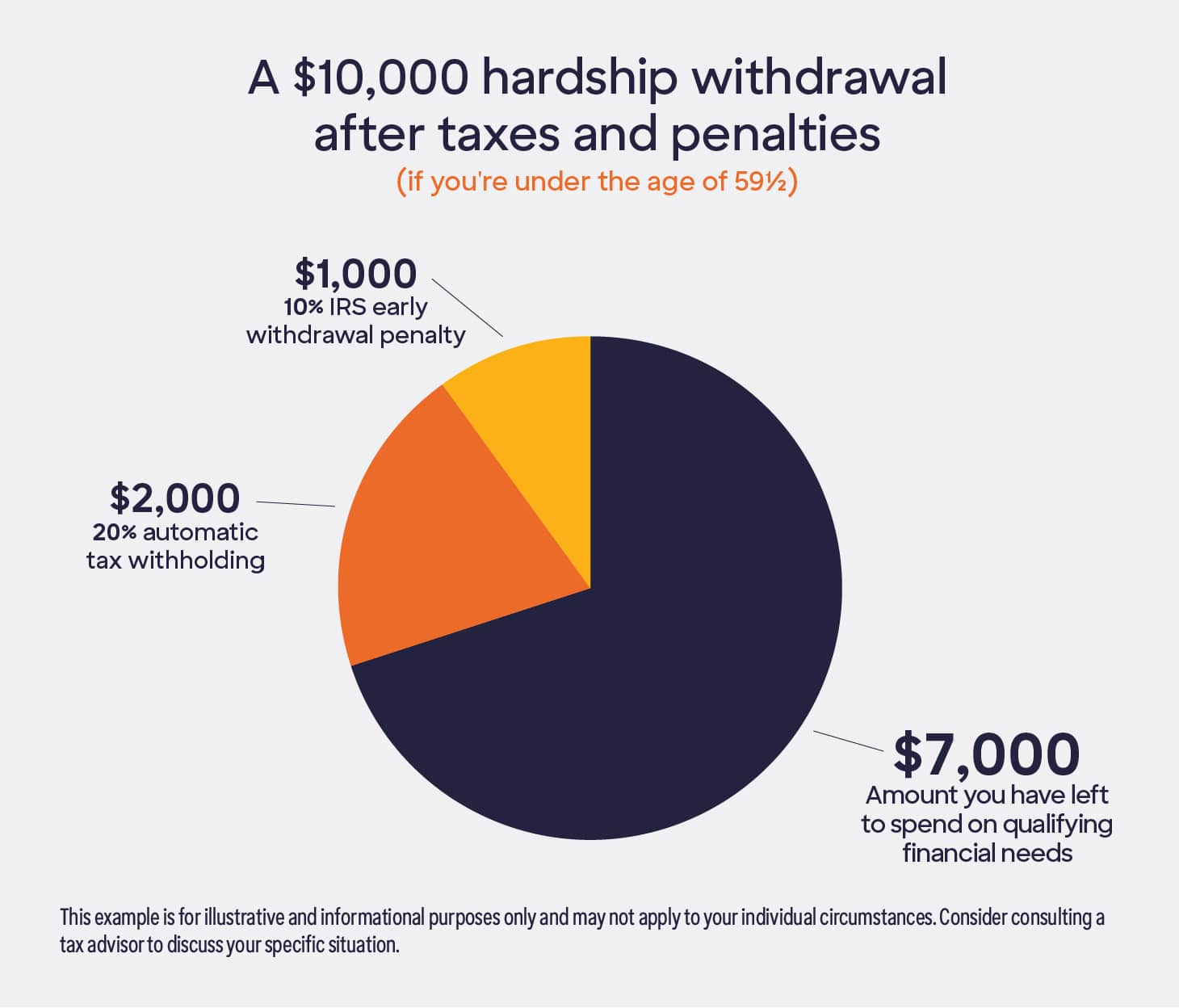

A 401(k) hardship withdrawal allows participants to withdraw funds from their retirement accounts to meet an immediate and heavy financial need. The Internal Revenue Service (IRS) has specific guidelines that outline what constitutes a qualifying hardship. Generally, these include expenses related to purchasing a primary residence, medical expenses, tuition and educational fees, and preventing eviction or foreclosure.

It is important to note that hardship withdrawals are not loans; the money withdrawn is removed from the account permanently and is subject to taxes and potential penalties. Understanding the nuances of this process is essential for making informed decisions regarding your retirement savings.

Qualifying Criteria for Hardship Withdrawals

To qualify for a hardship withdrawal, you must demonstrate that you have an immediate financial need and that the amount withdrawn is necessary to satisfy that need. The following criteria typically apply:

- Unpaid medical expenses for you, your spouse, or dependents.

- Costs related to the purchase of a primary residence.

- Payments to prevent eviction or foreclosure on your primary home.

- Tuition and educational fees for the upcoming academic period.

- Funeral expenses for a family member.

Eligibility Requirements for Hardship Withdrawals

While the IRS sets the overarching rules for hardship withdrawals, employers may impose additional requirements. Typically, you must meet the following criteria:

- You must be a participant in the 401(k) plan.

- You must have exhausted all other sources of funding, including loans from your 401(k).

- Your need must be immediate and severe.

Documentation Needed

When applying for a hardship withdrawal, you will need to provide documentation that supports your claim. This may include:

- Invoices or bills for medical expenses.

- Purchase agreements for a primary residence.

- Eviction notices or foreclosure documents.

The Role of Employers in 401(k) Hardship Withdrawals

Employers play a critical role in the administration of 401(k) plans, including the approval of hardship withdrawals. Each employer may have specific policies and procedures for processing these requests. It is essential to understand how your employer’s plan defines hardship and what documentation is required for approval.

Additionally, employers have the right to deny a hardship withdrawal if they believe the request does not meet the criteria set forth by the IRS or their own plan rules. As such, transparency and honesty in your application are paramount.

Consequences of Lying to Get a Hardship Withdrawal

Lying to obtain a 401(k) hardship withdrawal can have severe consequences. If you are found to have provided false information, you may face:

- Immediate repayment of the withdrawn funds.

- Tax penalties and interest on the amount withdrawn.

- Potential legal action from your employer or the IRS.

Moreover, dishonesty can lead to a loss of trust with your employer and can impact your future employment opportunities. The risks far outweigh any short-term financial relief that might be gained through deception.

Alternatives to Hardship Withdrawals

If you are facing financial difficulties but are hesitant to apply for a hardship withdrawal, there are alternative options to consider:

- **401(k) Loans**: Depending on your employer’s plan, you may be able to take a loan against your 401(k) balance. This option allows you to borrow money without incurring taxes or penalties, provided you repay the loan within the specified timeframe.

- **Emergency Savings Fund**: Building an emergency fund can provide a financial cushion for unexpected expenses, reducing the need to access retirement savings.

- **Personal Loans**: Consider obtaining a personal loan from a bank or credit union. These loans typically have lower interest rates than credit cards.

How to Apply for a Hardship Withdrawal

Applying for a 401(k) hardship withdrawal involves several steps, including:

- Review your employer’s 401(k) plan documents to understand the rules regarding hardship withdrawals.

- Gather documentation that supports your financial need.

- Complete the necessary application forms provided by your employer or plan administrator.

- Submit your application along with the required documentation.

Expert Views and Statistics

Financial experts emphasize the importance of adhering to ethical standards when it comes to retirement savings. According to a recent survey by the Employee Benefit Research Institute (EBRI), approximately 20% of 401(k) plan participants have considered taking a hardship withdrawal. However, many experts warn against the potential long-term consequences of depleting retirement savings for immediate needs.

Statistics show that individuals who take early withdrawals from their 401(k) plans often struggle to rebuild their retirement savings. In fact, the average balance of individuals who withdraw from their 401(k) is significantly lower than those who do not.

Conclusion

In conclusion, the temptation to lie for a 401(k) hardship withdrawal can be strong, especially in times of financial distress. However, the risks and potential consequences far outweigh any perceived benefits. It is crucial to understand the rules and regulations surrounding hardship withdrawals and to approach the process with honesty and integrity. If you find yourself in need of financial assistance, consider exploring alternative options and seek guidance from financial professionals. Remember, preserving your retirement savings is essential for your long-term financial health.

We encourage readers to share their thoughts and experiences related to 401(k) hardship withdrawals in the comments below. If you found this article helpful, consider sharing it with others who may benefit from this information.

Thank you for reading, and we hope to see you back for more insightful articles on financial topics!

Exploring The De La Cruz Bat Knob: A Unique Fusion Of Art And Functionality

Exploring The Enigmatic Ship Cemetery Of Bangladesh

Understanding IPhone Battery Draining: Causes, Solutions, And Tips For Longevity